Across Africa and MENA, businesses are moving away from slow, expensive payment systems. Crypto payment use cases are reshaping how workers send money home, how freelancers get paid, and how companies settle transactions.

We at Web3 Enabler have seen firsthand how cryptocurrency cuts costs and speeds up payments in these regions. This post shows real examples of how it works.

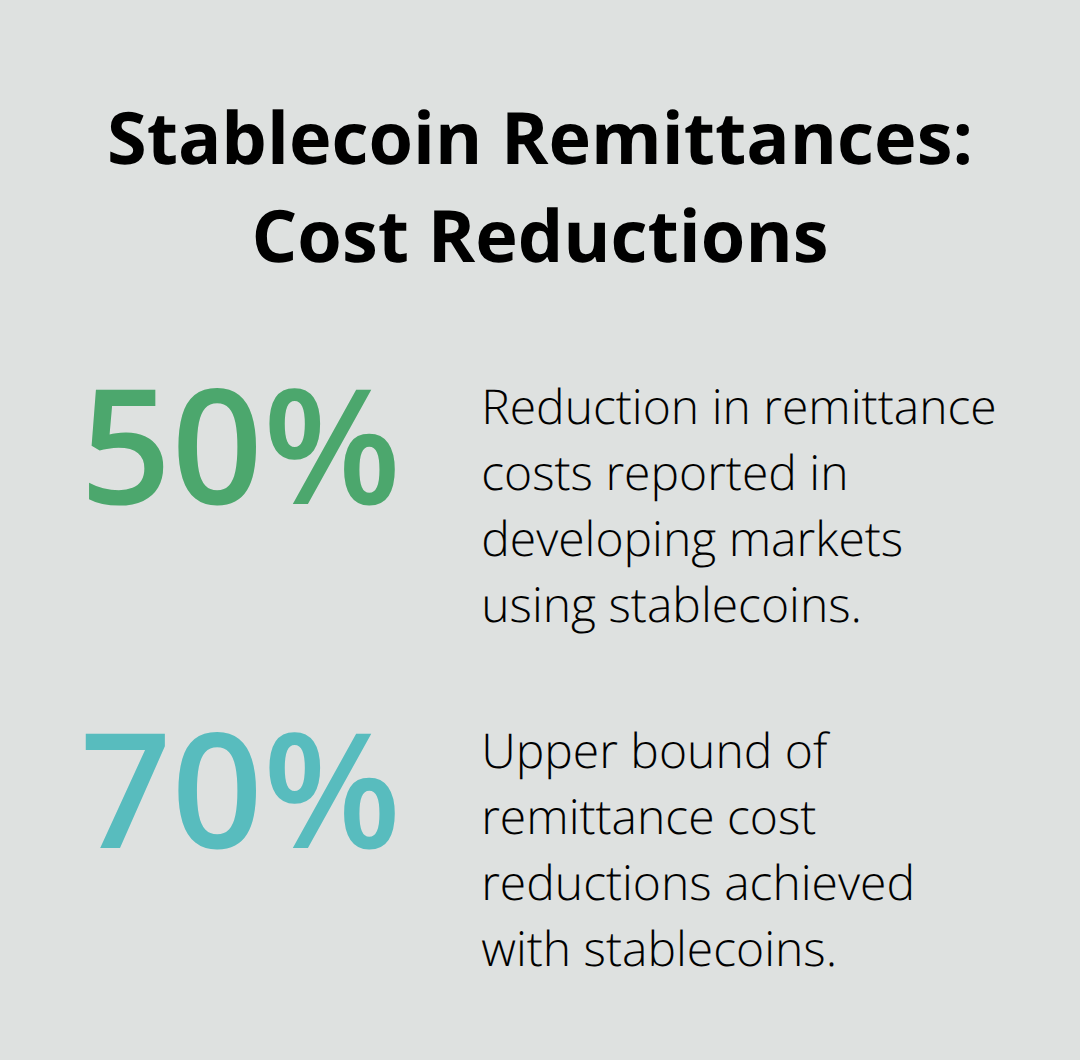

How Crypto Cuts Remittance Costs in Half

African workers sending money home face a brutal reality: traditional wire transfers cost no more than 3% for a $200 transfer. Over a year, a worker in the diaspora sending $200 monthly to family loses significantly less to fees than before. Stablecoins change this equation entirely. A remittance via USDT or USDC costs a fraction of a percent, with settlement in minutes instead of days. Stablecoins have already reduced remittance costs by 50 to 70 percent in developing markets, and Nigeria processed approximately $22 billion in stablecoin transfers between July 2023 and June 2024. This volume climbs because workers see the math immediately. A $200 transfer that costs under $6 through a bank costs under $1 on-chain. That difference matters when you support a family on limited income.

The Mechanics of Faster Transfers

The process works without intermediaries or hold periods. A worker in London converts pounds to USDC, sends it to a recipient’s wallet in Lagos, and the recipient converts it to naira within an hour. No hidden fees buried in exchange rates. The recipient gets real-time notification and accesses funds 24/7, not just during banking hours. Speed transforms the experience. A traditional remittance takes three to five business days. A stablecoin transfer settles in minutes. For someone waiting to pay rent or cover an emergency, minutes versus days means the difference between solving the problem and falling behind.

Where the Volume Concentrates

West Africa dominates stablecoin remittance activity. Nigeria alone accounts for roughly 40% of stablecoin inflows across Sub-Saharan Africa, with 25.9 million digital asset users participating in the ecosystem. Ethiopia posted 180% year-over-year growth in retail stablecoin transfers after a currency devaluation, showing how workers pivot to crypto when local currency stability collapses. East Africa catches up fast. Kenya ranks fifth globally for stablecoin transactional use, supported by existing mobile money infrastructure like M-Pesa, which means workers already understand the on-ramp process. The pattern holds consistent: wherever traditional remittance costs run highest and banking access remains weakest, stablecoin adoption accelerates. Remittance flows to Africa totaled about $54 billion in 2023, and stablecoins capture an increasing share because the cost advantage proves undeniable. A worker sending $500 monthly saves nearly $1,000 per year switching to stablecoins. Multiply that across millions of workers, and the economic impact reshapes household finances across the region.

Removing the On-Ramp Friction

The friction point isn’t the stablecoin transfer itself-it’s converting local currency to USDC without losing money to excessive markups or waiting days for bank transfers. Local operators solve this problem. In Nigeria, platforms like Luno and Busha provide straightforward on-ramps. In Kenya, integration with M-Pesa means a worker funds a stablecoin transfer directly from their phone. For recipients, the reverse applies: they need quick access to local currency without selling stablecoins at unfavorable rates. A practical setup pairs stablecoins with a regulated exchange or fintech that offers fast conversion back to naira, shilling, or other local currencies. The operational simplification alone cuts costs and reduces settlement risk. A well-designed system removes the barriers that make crypto feel complicated. Workers already use mobile money daily, so adding stablecoin capability to that experience feels natural rather than foreign. This integration matters because it transforms crypto from a technical novelty into a tool that fits existing payment habits.

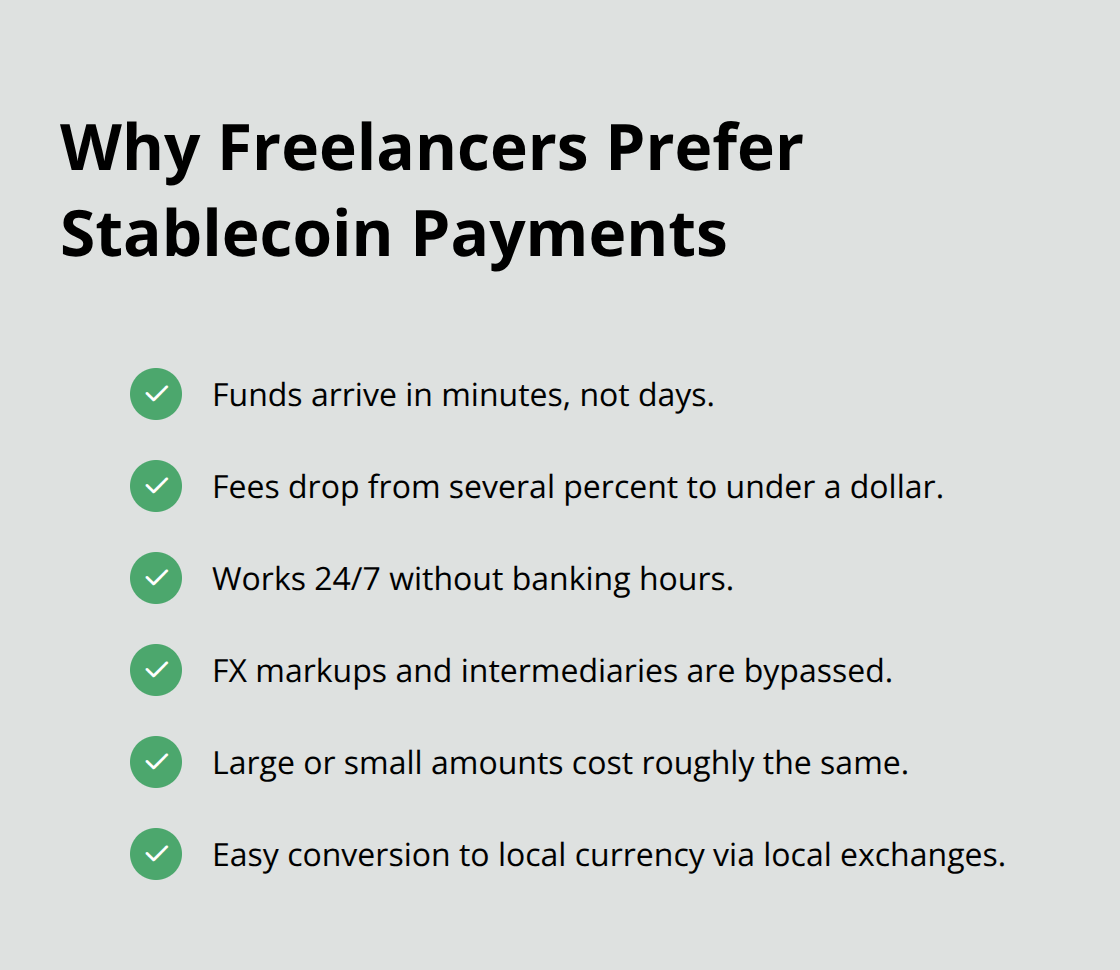

Freelancers and E-Commerce Sellers Getting Paid Faster

Freelancers across MENA face a payment reality that traditional systems cannot solve. A designer in Cairo takes on work from a US agency and waits five to seven business days for wire transfer funds to arrive, only to lose 3 to 5 percent of the total to hidden FX markups and intermediary fees. A seller on an e-commerce platform ships goods from Morocco to Europe and watches payment processors hold funds for 14 days while currency conversion happens at unfavorable rates. Stablecoins eliminate these delays entirely. A client sends USDC directly to a freelancer’s wallet, settlement happens in minutes, and the freelancer converts to local currency immediately through a local exchange without waiting for banking hours or intermediary approvals. The math changes everything. A freelancer earning $2,000 monthly loses between $120 and $300 to traditional payment friction. Over a year, that amounts to $1,440 to $3,600 in lost income simply for the privilege of getting paid. Stablecoin transfers cost less than $1 per transaction regardless of amount, meaning a $2,000 payment costs the same as a $20,000 payment.

This cost structure makes crypto payments economically rational for anyone earning above $500 monthly, and most professional freelancers far exceed that threshold. Kenya ranks fifth globally for stablecoin transactional use, and much of that activity comes from freelancers and small business owners receiving international payments. The infrastructure exists because the demand is real and the pain is measurable.

Global Companies Prefer Stablecoin Payments

Global companies increasingly prefer paying contractors in stablecoins rather than managing multiple wire transfer corridors. A software firm in Berlin hires developers across Egypt, Tunisia, and Lebanon and discovers that paying each contractor in local currency requires separate bank relationships, compliance reviews, and settlement windows. Paying all three in USDC simplifies the process dramatically. One transfer, one compliance check, and each developer receives funds in their preferred stablecoin within minutes. They then convert to local currency through established local providers. For the hiring company, this approach reduces payment overhead and eliminates the FX hedging complexity of maintaining multiple currency positions. Freelancers and small business owners should recognize this shift and position themselves as stablecoin-ready. A freelancer lists USDC as an accepted payment method on their portfolio or proposal and immediately signals professional maturity and technical competence to international clients. This positioning alone can justify a small premium in rates because clients recognize the reduced operational burden.

E-Commerce Sellers Accelerate Cash Flow

E-commerce sellers shipping goods internationally face similar advantages. A retailer in South Africa sells to customers across MENA and accepts payment in USDC, eliminating the need to hold multiple currencies or wait for cross-border settlement. Inventory replenishment from suppliers in Nigeria happens faster when both parties use stablecoins, reducing working capital tied up in payment delays. The practical effect compounds: faster payments improve supplier relationships, better payment terms become possible, and cash flow improves. These businesses should integrate stablecoin payment options directly into their checkout experience, not as an afterthought. Platforms like Transak provide the on-ramp and off-ramp infrastructure needed to make this seamless for customers and merchants alike, handling KYC, AML compliance, and currency conversion in the background.

Building Operational Confidence in Crypto Payments

The barrier preventing wider adoption among freelancers and e-commerce operators is not technical complexity but operational confidence. Most payment systems require new workflows, compliance considerations, and currency management disciplines that feel unfamiliar. The solution treats stablecoin payments as a specific tool for specific problems rather than a complete payment system overhaul. A freelancer accepts stablecoins from international clients while continuing to accept local bank transfers from regional clients. An e-commerce seller offers stablecoin checkout to wholesale buyers while maintaining traditional payment methods for retail customers. This phased approach reduces risk and allows operators to learn the process without betting their entire business on a new system.

Selecting the Right Stablecoin and Exchange Partner

Practical implementation starts with selecting a stablecoin with real liquidity in your region. USDT remains dominant across Africa and MENA due to accessibility and established exchange relationships. USDC offers regulatory advantages in jurisdictions like Kenya where regulatory clarity is accelerating. The choice matters because it determines how easily you convert to local currency without slippage or unfavorable pricing. Next, establish a relationship with a local exchange or fintech that handles conversion reliably. In Nigeria, platforms like Luno and Busha provide straightforward conversion. In Egypt or UAE, established crypto exchanges handle large-volume conversions at fair rates. Finally, implement clear accounting practices to track crypto transactions alongside traditional payments. Most accounting software now supports cryptocurrency transactions, removing the excuse that crypto payments complicate financial reporting. The operational setup takes two weeks, not two months. Freelancers and e-commerce operators who move first gain a competitive advantage because they can accept payments faster, cheaper, and more reliably than competitors still reliant on traditional banking corridors. This foundation positions them well for the next phase: how larger enterprises and real estate transactions leverage blockchain infrastructure to settle complex deals with speed and transparency.

How Blockchain Settles Large Deals Faster Than Banks

Corporate treasury teams and real estate firms across Africa and MENA are discovering that blockchain infrastructure solves problems traditional banking cannot address. A property developer in Dubai tokenizing real estate assets into tradeable shares, starting February 20, 2026, demonstrates how blockchain creates fractional ownership and secondary markets that didn’t exist before. The Dubai Land Department’s Phase II rollout will release approximately 7.8 million real estate tokens available for resale, lowering entry barriers for first-time investors and allowing token holders to sell smaller stakes for liquidity without waiting months for buyers. This shift matters for corporate payments too. When a South African manufacturer settles supplier invoices across Nigeria and Egypt, traditional wire transfers require navigating three separate banking corridors, compliance reviews for each jurisdiction, and settlement windows spanning five to seven days. Stablecoin transfers compress this to minutes. A company paying suppliers $500,000 across multiple countries via USDC settles each payment in one transaction, converting to local currency through established local exchanges without intermediary delays. The cost difference proves substantial: traditional cross-border B2B payments in Africa cost 6 to 10 percent in fees, while stablecoin transfers cost under 0.1 percent. For large transactions, this gap justifies immediate implementation. Corporate stablecoin transfers grew 25 percent in 2024, signaling rising adoption in treasury management, payroll, and supplier payments.

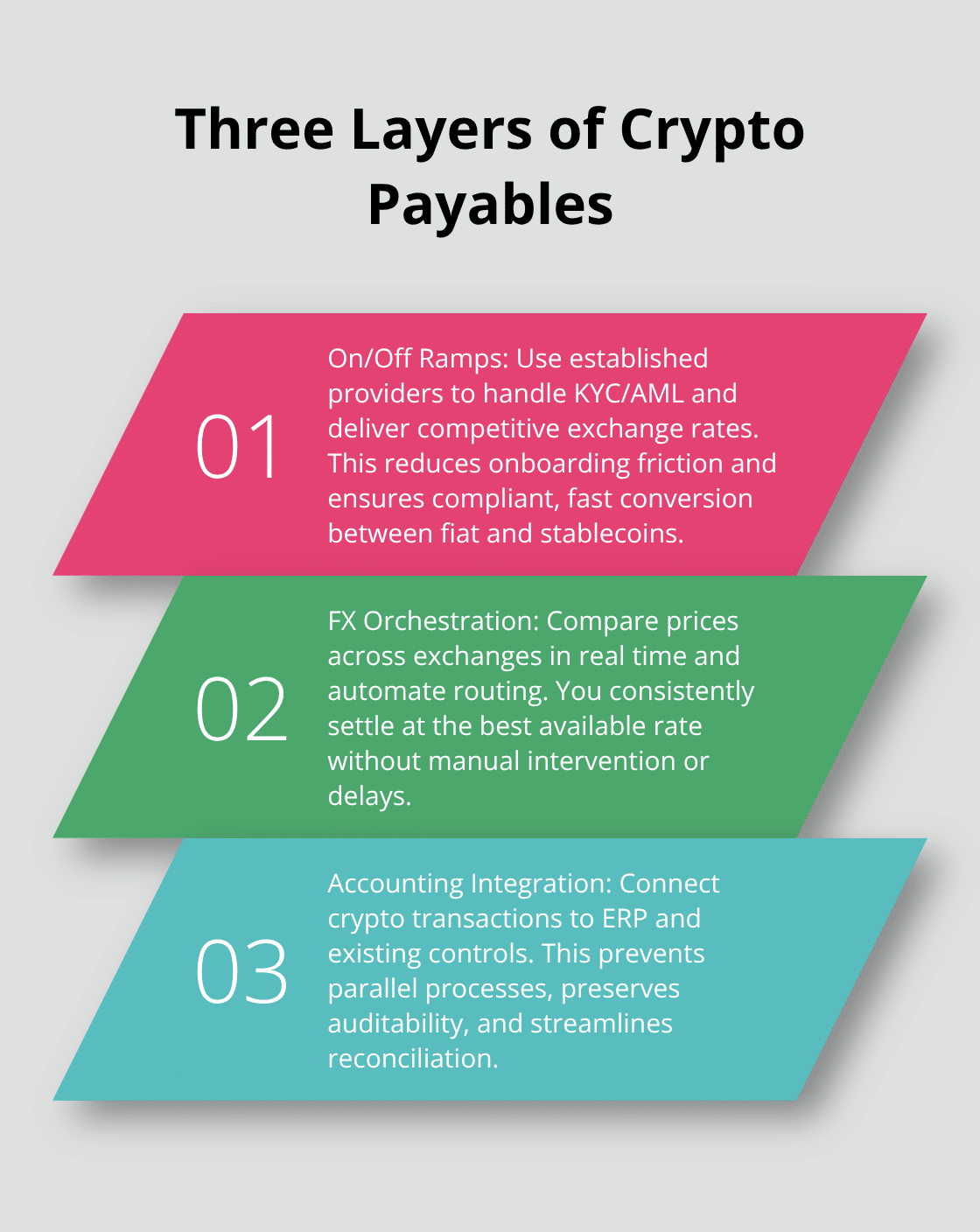

Structure Crypto-Based Payables Around Three Operational Layers

Companies should organize crypto-based payables around three operational layers. First, implement robust on-and-off ramps through established providers like Transak, which handle KYC and AML compliance in the background while delivering competitive exchange rates. Second, deploy FX orchestration tools that compare stablecoin pricing across exchanges in real time, ensuring you settle at the best available rates without manual intervention. Third, integrate crypto transactions directly into your accounting and ERP systems so payments flow through your existing financial controls without creating parallel processes that complicate audit trails.

Blockchain-Based Title Management Eliminates Transfer Delays

Property transfers in Africa and MENA traditionally require government offices, lawyers, and weeks of processing before title passes legally. Blockchain-based title management compresses this timeline dramatically. Dubai’s tokenization framework partners the Virtual Assets Regulatory Authority with the Land Department, ensuring tokens link directly to official title deeds. A buyer purchasing a tokenized property share owns a verified fraction of the asset with full legal standing. The resale market creates controlled secondary trading, allowing investors to exit positions without waiting for a single buyer to emerge for the entire property. For businesses acquiring commercial real estate or managing property portfolios, this represents operational efficiency. A company in Cairo acquiring multiple warehouse properties can settle purchases in stablecoins, receive tokenized title shares immediately, and begin generating rental income without waiting for traditional conveyancing. The speed advantage compounds when managing cross-border acquisitions. A South African firm expanding into Kenya can purchase commercial property, receive blockchain-verified title, and execute a supply agreement with a local partner using the same stablecoin infrastructure that powered the property acquisition. One compliance framework. One settlement network. Multiple transactions across different asset classes.

Supplier Payments Consolidate Currency Exposure

Large enterprises across the region face currency exposure when maintaining supplier relationships in multiple countries. A manufacturing firm in South Africa paying component suppliers in Nigeria, Egypt, and UAE holds currency positions in three different markets, hedging costs, and exposure to sudden devaluations. Crypto-based payables consolidate this complexity. The company holds treasury reserves in stablecoins, pays suppliers in USDC, and each supplier converts to local currency through their preferred local exchange. The manufacturer’s FX exposure disappears because stablecoins eliminate currency volatility between payment and settlement. Each supplier manages local currency conversion at their preferred timing, removing the pressure to accept unfavorable rates imposed by traditional banking corridors. This operational model works best when combined with proper accounting integration. Most enterprise accounting systems now support cryptocurrency transaction tracking, so your finance team records stablecoin payments in the same ledger as traditional bank transfers. The administrative burden disappears.

Implement Crypto Payables With a Pilot Program

Implementation requires selecting one primary stablecoin for corporate use (USDC offers regulatory advantages in Kenya and increasingly across the region), establishing direct relationships with two or three local exchanges that handle large-volume conversions at institutional rates, and testing the workflow with a pilot program involving one or two suppliers before rolling out company-wide. The pilot phase reveals operational friction and allows your team to refine processes without disrupting your entire supply chain. Most companies complete this pilot within four weeks and see immediate improvement in settlement speed and cost reduction.

Final Thoughts

The evidence across Africa and MENA proves that crypto payment use cases have shifted from experimental to operational. Workers send remittances home in minutes instead of days, losing a fraction of what traditional banks extract. Freelancers and e-commerce operators accept international payments without waiting for banking corridors to process transfers. Corporate teams settle supplier invoices across multiple countries using stablecoins, eliminating currency exposure and reducing costs from 6 to 10 percent down to under 0.1 percent.

For businesses ready to act, the path remains straightforward. Select a stablecoin with real liquidity in your market (typically USDT or USDC depending on your jurisdiction), establish relationships with one or two local exchanges that handle conversions reliably at institutional rates, and integrate crypto transactions into your existing accounting systems. Most companies complete this setup within four weeks and see immediate improvement in settlement speed and cost reduction.

We at Web3 Enabler help businesses integrate crypto payments into their existing infrastructure. Our platform connects blockchain transactions directly to Salesforce, making crypto accessible without replacing your current systems. The businesses winning in Africa and MENA aren’t waiting for perfect conditions-they implement crypto payments now, learn from real transactions, and build competitive advantages through faster settlements and lower costs.