Your checkout process is bleeding money. International customers abandon carts at alarming rates because traditional payment methods are slow, expensive, and frankly, a pain.

Stablecoin payments for ecommerce fix this. We at Web3 Enabler have seen firsthand how instant, borderless transactions transform customer experience and your bottom line.

Why Stablecoins Beat Traditional Checkout

The numbers don’t lie. Traditional cross-border payments charge merchants between 2–7% in fees, with settlement taking three to five business days. International remittances average over 6% in costs, according to industry data. Meanwhile, stablecoin transfers settle in minutes or seconds with network fees often under a dollar. Between October 2024 and October 2025, stablecoins processed $9 trillion in adjusted payment activity, up 87% year over year. That’s not hype-that’s real money moving faster and cheaper than any card network can offer.

Your Customers Already Know the Difference

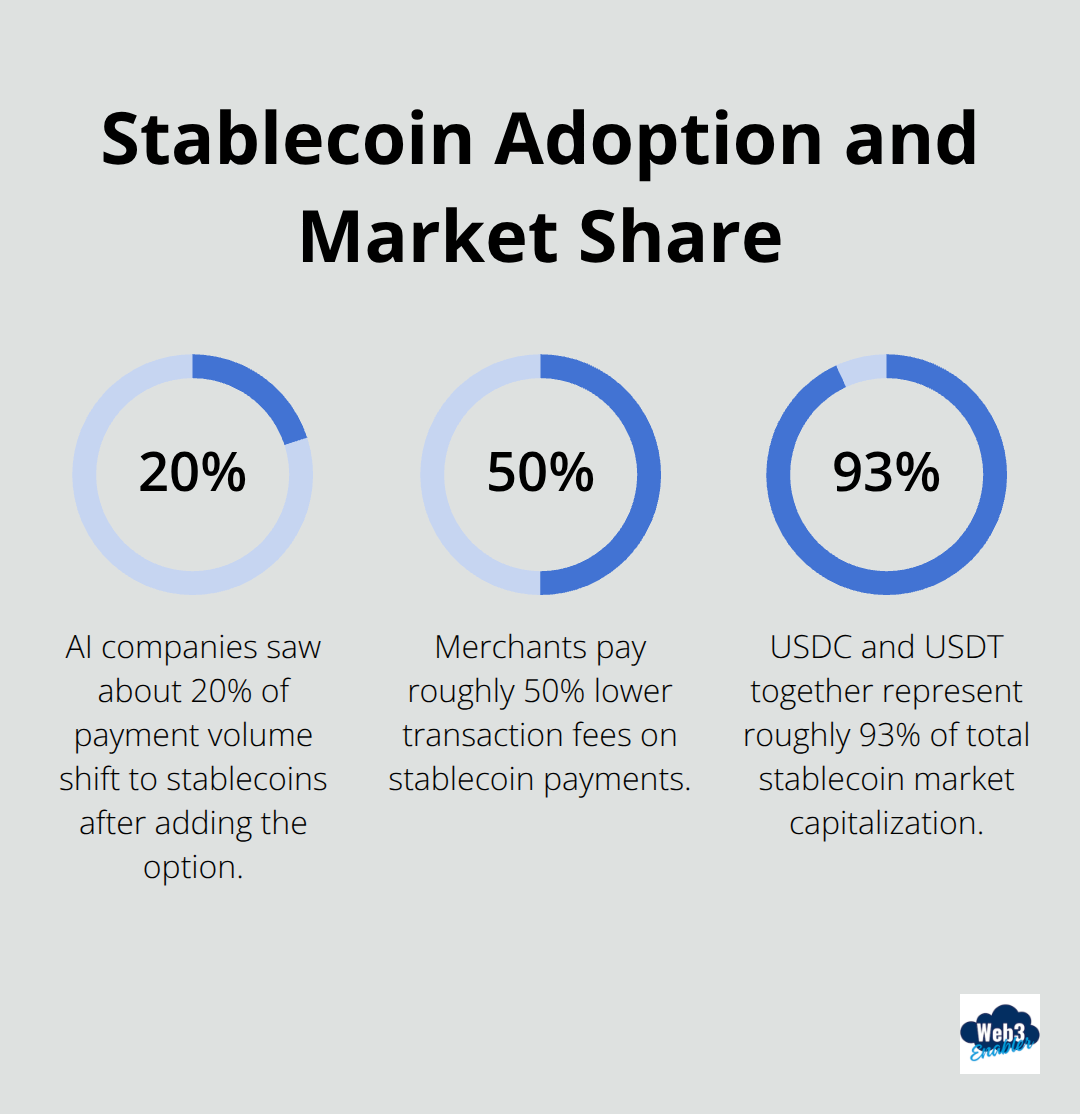

Your customers feel the friction of waiting for funds to clear, watching exchange rates swing, and paying fees that feel arbitrary. When they see stablecoins as an option, they take it. AI companies have reported roughly 20% of payment volume shifting to stablecoins after adding the option, and Stripe users experience about lower transaction fees on stablecoins versus other methods.

The checkout experience itself matters too. Stablecoin payments let customers with crypto wallets sign a transaction directly-no card details, no middlemen, no three-day clearing period. The blockchain handles settlement with finality, meaning no chargebacks and no disputes dragging on for weeks. Your cash flow improves immediately, inventory restocking accelerates, and you can reinvest faster.

Global Liquidity Never Sleeps

Traditional banking closes. Stablecoins don’t. Settlement happens 24/7, which means your suppliers in Asia, partners in Europe, and freelancers in Latin America receive payments instantly, regardless of the time zone or local banking hours. This matters especially for marketplaces and ecommerce platforms managing inventory across multiple regions. Faster payouts reduce working capital cycles and improve supplier relationships.

Regulatory Backing Builds Confidence

The regulatory environment finally caught up. The GENIUS Act, signed in July 2025, creates a U.S. framework requiring stablecoins to be backed 1:1 by reserves and sets monthly disclosure requirements. The EU’s MiCA regulation, rolled out across member states in 2025, enforces similar 1:1 backing standards. These frameworks reduce counterparty risk and give merchants confidence that the stablecoins they accept won’t collapse overnight.

When you accept USDC or USDT (which together account for roughly 93% of total stablecoin market capitalization), you accept digital dollars backed by real reserves and governed by real oversight. This regulatory clarity transforms stablecoins from a speculative asset into a legitimate payment rail-one that integrates seamlessly with your existing checkout infrastructure.

How Stablecoin Payments Actually Work

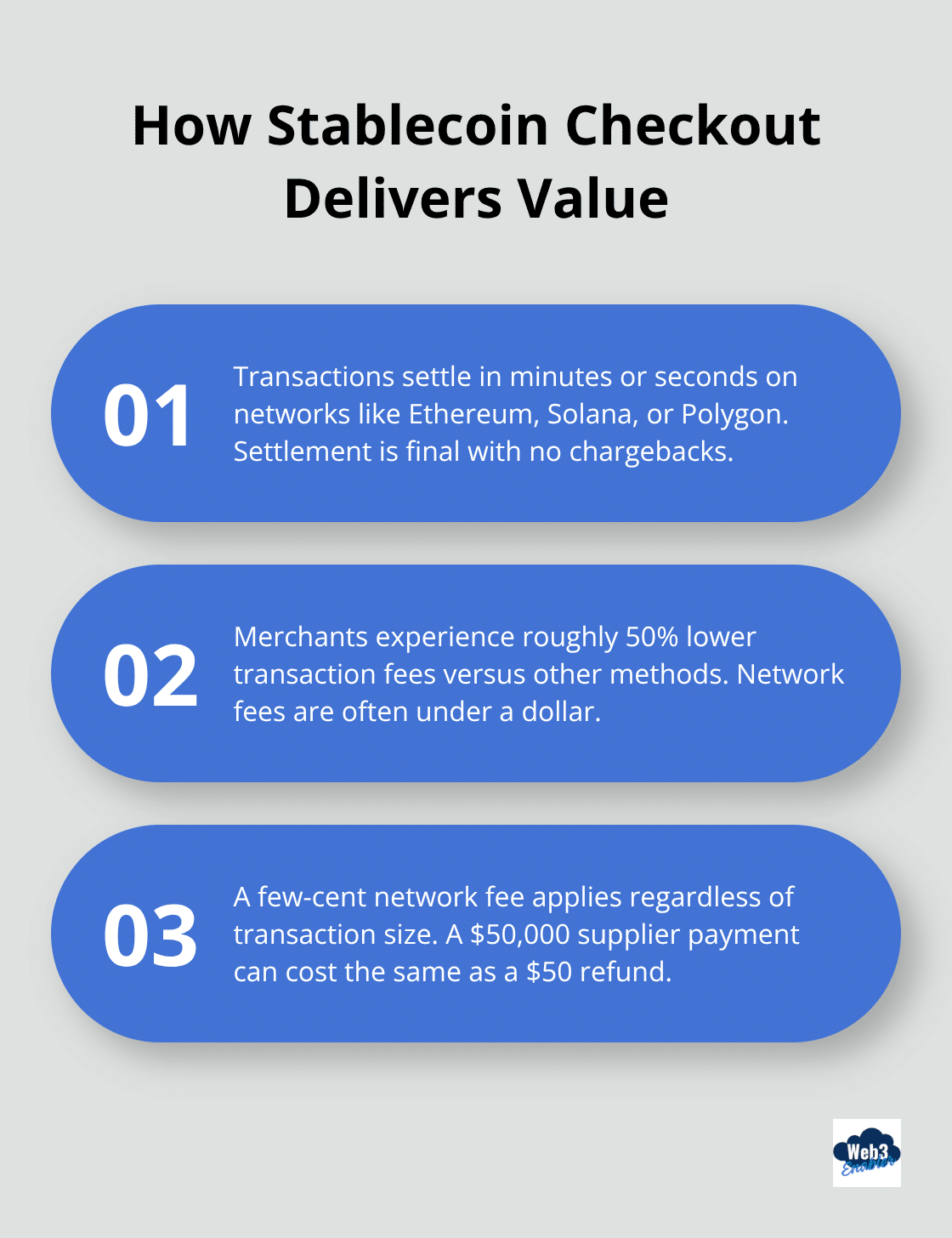

Stablecoins are digital tokens pegged 1:1 to fiat currency, typically the US dollar. When a customer checks out with a stablecoin, they send a real asset backed by real reserves held by issuers like Circle (USDC) or Tether (USDT). The transaction broadcasts to a blockchain network-Ethereum, Solana, or Polygon being the most common-and settles in minutes or seconds. Settlement is final. No chargebacks. No disputes lingering for weeks while your cash sits in limbo. Merchants experience roughly 50% lower transaction fees on stablecoins compared to other methods, and that cost advantage compounds across thousands of transactions.

The network fee itself runs just a few cents, regardless of transaction size, making a $50,000 supplier payment cost the same as a $50 customer refund.

Getting Stablecoins Into Your Checkout Flow

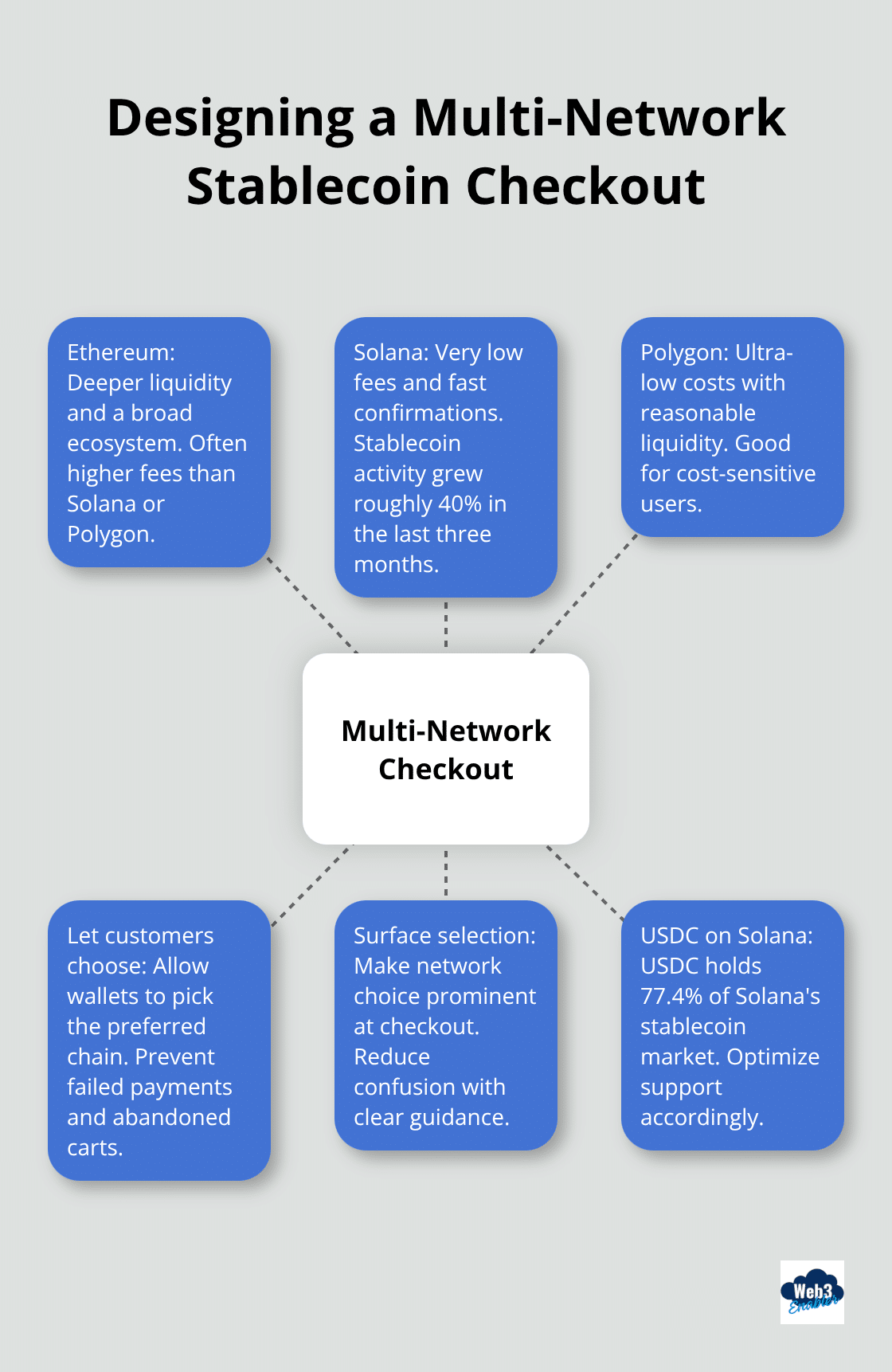

Integration doesn’t require you to reinvent your entire payment stack. Providers like Stripe handle the complexity by accepting stablecoins across multiple networks and settling directly to your bank account in local currency. You add one integration and suddenly customers with crypto wallets can pay with USDC on Ethereum, Solana, or Polygon without you worrying about which blockchain they prefer. The checkout experience uses wallet connectivity like WalletConnect or simple QR codes-customers sign the transaction in their wallet and move on. No card forms. No PCI compliance headaches. Support multiple networks because your customers are fragmented across them. Solana’s stablecoin activity grew roughly 40% in the last three months while Ethereum remains the larger ecosystem overall, according to transaction volume data. Forcing customers onto a single network guarantees you’ll lose payment volume.

Why Settlement Speed Changes Your Business Model

On-chain settlement works differently from traditional banking. Your money arrives and it’s yours. No pending status. No intermediary banks taking three days to move funds between accounts. This matters most for high-volume operations and cross-border scenarios. Marketplaces pay out to thousands of sellers instantly rather than batching them for overnight settlement. A freelancer in Argentina receives payment from a US client in minutes, not days, which improves cash flow for both parties and eliminates the working capital gap that traditional banking creates. Between October 2024 and October 2025, stablecoins processed $9 trillion in adjusted payment activity, reflecting real businesses using this infrastructure for actual payments, not speculation.

Regulatory Certainty Protects Your Operations

The regulatory environment supports stablecoin payments now. The GENIUS Act requires 1:1 backing and monthly disclosures, while MiCA across the EU enforces similar standards. That regulatory certainty means you’re not betting on some experimental asset-you’re using payment rails governed by actual oversight. When you accept USDC or USDT (which together account for roughly 93% of total stablecoin market capitalization), you accept digital dollars backed by real reserves and governed by real oversight. This framework transforms stablecoins from a speculative asset into a legitimate payment rail that integrates seamlessly with your existing checkout infrastructure.

Now that you understand how stablecoins move through your checkout, the real challenge emerges: managing multiple networks, compliance requirements, and customer expectations across different regions.

Building a Global Checkout Experience with Stablecoins

The moment you decide to accept stablecoins, fragmentation hits hard. Your customers live across Ethereum, Solana, and Polygon. USDC dominates Solana with 77.4% of that ecosystem’s stablecoin market, while Ethereum remains the larger network overall in absolute terms.

Force everyone onto a single chain and you lose payment volume. The practical move supports multiple networks from day one, but this creates real operational complexity. You need clear customer guidance on which networks you accept, robust wallet connectivity through tools like WalletConnect, and a checkout flow that lets customers pick their preferred chain without confusion.

Many merchants bury network selection in technical settings, when it should live front and center at checkout. If your customer holds USDC on Solana but your integration only accepts Ethereum, that transaction fails and they abandon the cart. Accepting stablecoins across networks and settling fiat directly to your bank account eliminates the need for you to manage custody or multi-chain complexity yourself.

Network Economics Shape Customer Behavior

The network fee differences matter more than most merchants realize. Solana stablecoin activity grew roughly 40% in the last three months compared to Ethereum’s 27% growth, partly because transaction costs run pennies cheaper. Your customers notice these economics and route accordingly. Support their preference or watch them choose competitors who do.

Solana’s lower fees attract high-volume operations and price-sensitive customers. Ethereum offers deeper liquidity and broader ecosystem support. Polygon serves merchants seeking ultra-low costs with reasonable liquidity. Rather than picking one winner, accept all three and let customer wallets determine the flow. This approach maximizes payment volume across your customer base without forcing anyone into an economically suboptimal choice.

Compliance Becomes Your Regulatory Anchor

Regulatory frameworks finally provide real protection instead of uncertainty. The GENIUS Act, signed in July 2025, requires stablecoin issuers to maintain 1:1 reserve backing and publish monthly disclosures. The EU’s MiCA regulation, implemented in 2025, enforces identical standards across member states. This clarity means you’re not gambling on experimental assets-you’re using payment infrastructure governed by actual oversight.

When you accept USDC or USDT, which together represent roughly 93% of total stablecoin market capitalization, you accept dollars backed by audited reserves and regulatory scrutiny. Your compliance obligations depend on where your customers live. US-based operations need AML and sanctions screening, which blockchain analytics tools handle automatically. EU customers trigger MiCA compliance requirements around transaction monitoring and customer verification.

Rather than building compliance in-house, integrate specialized providers that handle blockchain analytics, sanctions screening, and KYC automatically. This keeps your operations clean without requiring a compliance team to become blockchain experts. Regional off-ramp differences also matter for your bottom line. Converting stablecoins to local currency varies dramatically by region-liquidity and bank integrations in Southeast Asia differ sharply from Latin America. Map your customer base by region first, then select stablecoin networks and settlement partners that support those specific markets.

Building Trust Through Transparency and Education

Customers don’t need crypto expertise to use stablecoin checkout. They need confidence that their money moves safely and arrives where it should. The best merchants treat stablecoins as a payment option, not as a technology lesson. Your checkout copy should emphasize outcomes-faster payouts, lower fees, instant settlement-rather than blockchain mechanics.

A simple message works: “Select stablecoin checkout to receive your payment in minutes instead of days.” No blockchain jargon required. Transparency about what stablecoins actually are matters more than most merchants realize. Explain that they’re digital dollars backed 1:1 by real reserves, governed by regulatory oversight, and settled instantly on blockchain networks. This positions stablecoins as boring infrastructure, not speculative assets. When customers understand this distinction, adoption rises.

Provide clear documentation about which networks you support and why you’ve chosen them. If you accept USDC on Ethereum and Solana but not Polygon, tell customers upfront. Ambiguity kills adoption faster than honest limitations. Some merchants worry that offering stablecoin checkout signals they’re experimental or crypto-focused. The opposite is true. Stablecoins processed $33 trillion in transaction volume during 2025, according to Artemis Analytics, a 72% year-over-year increase. This is mainstream infrastructure now, not a beta feature. Market it accordingly and watch payment volume shift toward stablecoin options, just as it has for AI companies reporting roughly 20% of payment volume moving to stablecoins after adding the option.

Final Thoughts

Stablecoin payments for ecommerce eliminate the friction that costs you customers and money. Traditional banking imposes arbitrary delays, unpredictable fees, and geographic boundaries that don’t match how modern commerce actually works. Stablecoins remove all three, giving your customers instant settlement and you lower costs while both of you skip the intermediaries that have been taking cuts for decades.

The regulatory frameworks now protect your operations. The GENIUS Act and MiCA provide the oversight that transforms stablecoins from experimental assets into legitimate payment infrastructure. When you accept USDC or USDT, you accept digital dollars backed by audited reserves and government scrutiny-this is infrastructure, not speculation. Stablecoins processed $33 trillion in transaction volume during 2025, up 72% year-over-year, and AI companies shifted roughly 20% of payment volume to stablecoins after adding the option, proving that real businesses solve real problems with this technology.

Getting started requires no blockchain expertise or payment stack rebuilds. You select a provider that handles the complexity, integrate it into your checkout, and let customers choose stablecoin payments alongside existing options. Web3 Enabler helps businesses connect blockchain technology with existing corporate infrastructure, enabling you to accept stablecoin payments, send global payments faster, and maintain full compliance visibility across your operations.