Your Salesforce instance handles customer data brilliantly. But what about payments? Fiat stablecoins in Salesforce change that game entirely.

We at Web3 Enabler have watched businesses waste thousands on slow cross-border transfers and clunky payment integrations. Stablecoins eliminate that friction. They settle in minutes, cost pennies, and play nicely with your existing ERP workflows.

Why Your Cross-Border Payments Cost More Than They Should

The Hidden Expense of Traditional Banking Rails

Traditional cross-border payments move money through a daisy chain of intermediaries, each taking a cut and adding delays. A wire transfer from the US to Southeast Asia takes three to five business days minimum. Your customer in Singapore waits. Your supplier in Manila waits. Your cash flow stalls. Meanwhile, correspondent banks skim fees at every handoff, sometimes charging 10–15 dollars per transaction on top of unfavorable exchange rates.

Stablecoins obliterate this friction entirely. They settle in minutes, not days. Costs drop to pennies per transaction. In 2024, stablecoins processed over 27 trillion dollars in transactions, surpassing Visa and Mastercard combined. That’s not hype-that’s the market voting with real money.

How Stablecoins Actually Work

Stablecoins are fiat-backed tokens that live on blockchain networks, meaning they inherit the speed and transparency of on-chain settlement while maintaining the price stability of the US dollar or other fiat currencies. No speculation, no volatility, just reliable money that moves at internet speed.

The reason enterprises increasingly adopt them is straightforward: they eliminate the friction that traditional rails create. Your Malaysian supplier receives value immediately without waiting for bank-to-bank currency conversions. Your working capital improves because settlement happens in minutes instead of days.

The Real Numbers on Speed and Cost

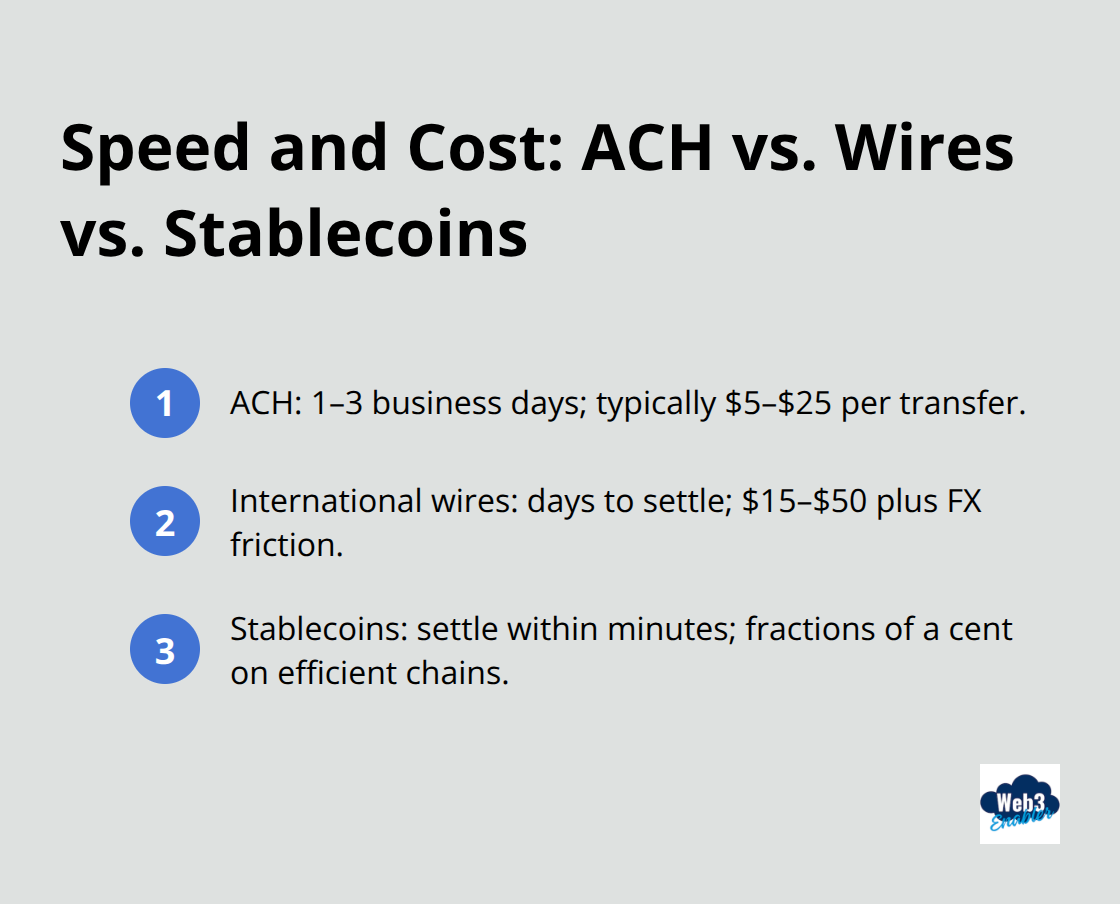

ACH transfers take one to three business days and typically cost five to twenty-five dollars per transaction. International wire transfers cost fifteen to fifty dollars and introduce foreign exchange friction on top. Stablecoin transfers settle within minutes with on-chain finality, costing fractions of a cent on Ethereum Layer 2 networks or other efficient chains.

For a company processing fifty cross-border supplier payments monthly, that’s potentially five hundred to fifteen hundred dollars in savings per month, or six thousand to eighteen thousand dollars annually-before you factor in the working capital advantage of faster settlement. If you’re paying contractors, vendors, or global team members through traditional rails, you’re leaving money on the table and frustrating your counterparties with delays.

Regulatory Frameworks Now Support Enterprise Adoption

Regulatory maturity matters here too. MiCA became fully effective in 2024 across the EU, the GENIUS Act is advancing in the US, and Hong Kong enacted its Stablecoin Ordinance in 2025. These frameworks establish clear rules around reserve backing, redemption rights, and governance, meaning the stablecoins you integrate into Salesforce aren’t flying blind-they’re backed by transparent compliance infrastructure.

Stripe Payments now facilitates stablecoin payouts alongside traditional methods, helping bridge fiat and crypto seamlessly. This shift signals that major payment processors recognize stablecoins as a legitimate complement to legacy systems, not a replacement. The infrastructure exists. The regulatory clarity exists. What remains is integrating these rails into your Salesforce environment-and that’s where the real operational advantage emerges.

Connecting Stablecoins to Salesforce Without the Headache

Salesforce handles your customer relationships and order data flawlessly, but it stops at the payment layer. That gap is where stablecoins fit in, and the good news is you don’t need a blockchain engineer to wire them in. Web3 Enabler offers 100% Salesforce Native solutions on the AppExchange that integrate stablecoin payments directly into your existing workflows without custom code or API wrestling matches. Stripe Payments already supports stablecoin payouts alongside traditional methods, and that infrastructure connects to Salesforce through standard integrations. When you set up a stablecoin payment flow, you add a faster, cheaper payment rail that your ERP already understands-no added complexity required.

Real-Time Data and Settlement

The Informatica and MuleSoft stack that Salesforce acquired integrates data from multiple sources in near real time, so your payment data flows seamlessly into your finance records without manual reconciliation. On-chain settlement creates a single immutable source of truth visible across your organization, which eliminates the opacity of multi-bank correspondent processes and drastically simplifies your audit trail. Real-time settlement also improves your working capital immediately-no waiting period for traditional payment rails to process through intermediaries.

Choose Your Stablecoins and Networks Upfront

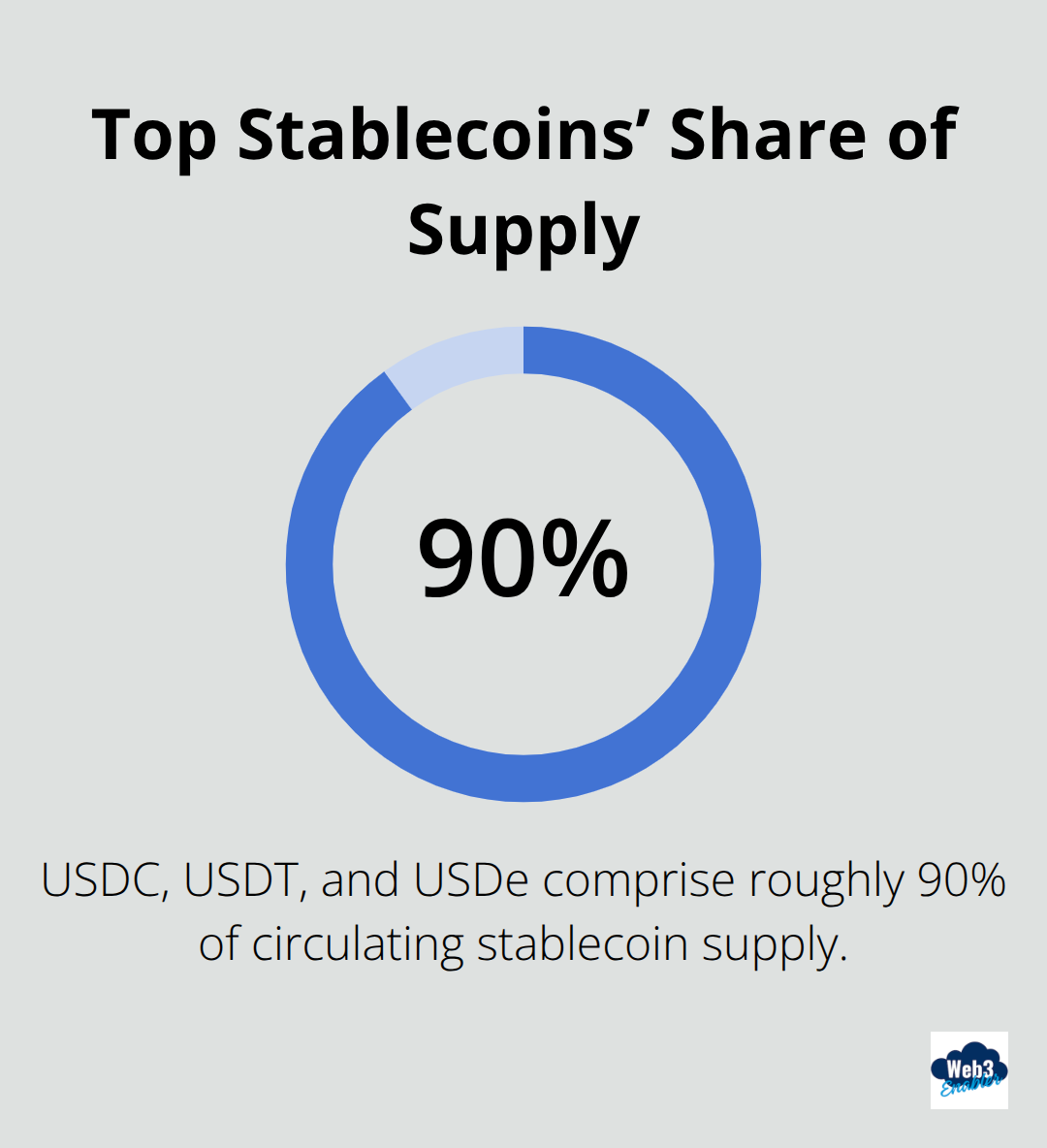

You need to decide which stablecoins you’ll accept and which blockchain networks you’ll use. USDC, USDT, and USDe make up roughly 90% of circulating stablecoin supply according to Deloitte Luxembourg, so starting with one of these three reduces operational complexity and ensures your counterparties can easily transact with you. You should also determine whether you’ll hold stablecoins directly or convert them to fiat upon receipt through automated options-this decision affects your tax reporting and exposure management.

Tax Reporting and Accounting

The IRS treats stablecoins as property, so you must report the USD value at receipt and track gains or losses on conversion. Your ERP tax module needs to handle this accounting at scale. Start with a pilot involving a single payout stream to a key supplier or contractor already open to stablecoins, then expand once you’ve validated the workflow and confirmed that your existing systems handle on-chain payment data correctly.

Error Handling and Compliance Checks

Stablecoin transfers settle within minutes with on-chain finality, which simplifies your reconciliation process compared to traditional rails, but you must implement robust error-handling since on-chain payments typically cannot be reversed once settled. Choose stablecoin issuers with transparent reserve backing and clear redemption rights, and ensure your vendor screening includes sanctions checks against blockchain addresses using blockchain analytics platforms. These compliance prerequisites protect your organization and align with regulatory frameworks now in place across the EU, US, and Hong Kong.

With your stablecoin infrastructure in place and your compliance stack validated, the real opportunity emerges: putting these faster payment rails to work across your actual business operations.

Where Stablecoins Actually Make Money for Your Business

Your global customer in Tokyo wants to pay you in stablecoins. Your supplier in Brazil needs faster payment without forex headaches. Your financial advisor clients hold crypto assets scattered across exchanges and wallets, invisible to your CRM.

These aren’t hypothetical scenarios-they’re happening now, and stablecoins solve them in ways traditional rails simply cannot. The stablecoin market hit 300 billion dollars in 2025, and annual transaction volume exceeded 27 trillion dollars in 2024, which means real businesses already move real money through these networks. The question isn’t whether stablecoins work; it’s whether you’re positioned to capture the operational and cash flow advantages they deliver.

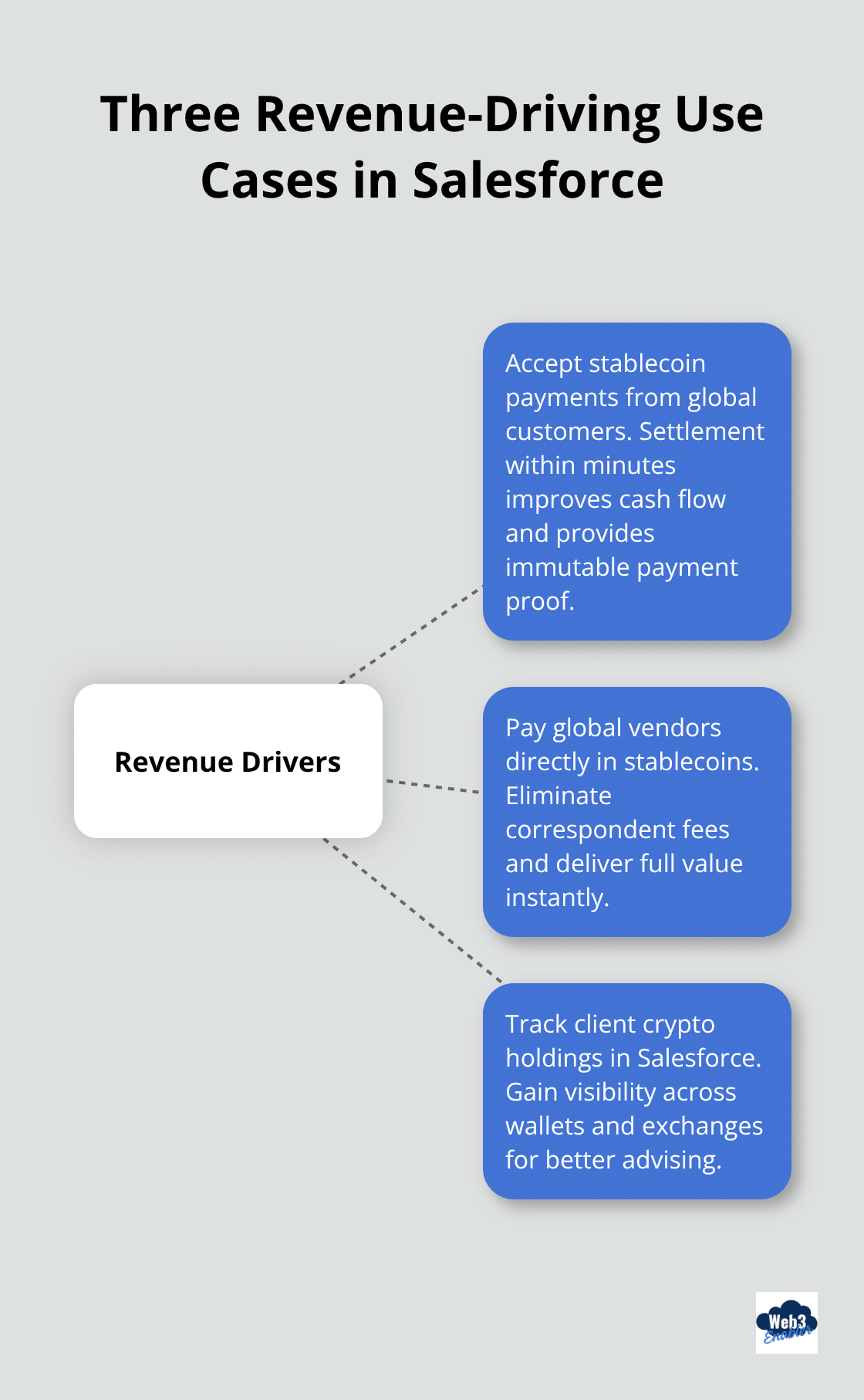

Accept Stablecoin Payments and Settle Faster Than Your Competitors

When a customer pays you via USDC or USDT, that transaction settles within minutes instead of one to three business days. Your cash flow improves immediately. Your customer knows the payment arrived because on-chain settlement creates immutable proof-no more chasing wire confirmations or reconciling mismatched reference numbers. For merchants processing high-volume international transactions, this matters enormously. A company receiving fifty customer payments monthly from across different countries saves five to fifteen days of float per transaction cycle. That’s working capital improvement without requiring additional inventory or operational changes.

You also sidestep foreign exchange friction entirely-a customer in Singapore sends USDC, you receive USDC, no currency conversion losses eating into your margin. The IRS treats stablecoins as property, so you report the USD value at receipt and track any gains or losses on conversion to fiat. Set up automated conversion through your payment processor if you prefer fiat exposure, or hold stablecoins directly if your treasury strategy supports it. Either way, your ERP captures the transaction data in real time, eliminating manual reconciliation work that traditionally bogs down your accounting team.

Pay Global Vendors Without the Correspondent Banking Tax

Paying a vendor in Manila or Mexico City through traditional wire transfer means correspondent banks take cuts at every handoff-sometimes 10 to 15 dollars per transaction on top of unfavorable exchange rates. A 10,000 dollar payment shrinks by 50 to 150 dollars before your vendor even touches it. Stablecoins eliminate this entirely. You send 10,000 USDC directly to your vendor’s wallet, they receive exactly 10,000 USDC within minutes, and your cost is fractions of a cent. For a company processing 50 vendor payments monthly across borders, that’s 6,000 to 18,000 dollars in annual savings before factoring in working capital gains from faster settlement.

More importantly, your vendors actually prefer this. They receive payment instantly without waiting for their bank to process international transfers, which means faster cash flow for them too. Start with one key supplier already open to stablecoins-someone you know and trust. Send a test payment through USDC or USDT, confirm the workflow in your ERP, then expand once you’ve validated that your systems handle payment data correctly.

Track Client Crypto Holdings in Your Salesforce Instance

Financial advisors managing client portfolios face a specific problem: crypto holdings scattered across exchanges, wallets, and custodians remain invisible to your Salesforce instance, creating blind spots in client relationship management and financial planning. A client holds 50,000 dollars in Bitcoin and Ethereum across three different platforms, but your CRM sees zero assets. You can’t track their total wealth, adjust recommendations, or identify upselling opportunities because the data doesn’t exist in your system.

Web3 Enabler’s Salesforce Native solutions pull client crypto holdings directly into your Salesforce environment, giving advisors complete visibility without manual spreadsheets or third-party tools. Your advisors see total assets under management across traditional and digital holdings, enabling better financial planning and more informed recommendations. This transparency also strengthens client relationships-advisors demonstrate they understand their clients’ full financial picture, not just the portion held in traditional accounts. Implementation takes days, not months, because the solution runs natively on Salesforce without custom code or API wrestling.

FAQ: Scaling Stablecoin Operations in Salesforce

How does the GENIUS Act change how I use stablecoins in the US?

As of April 2026, the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act has moved into a critical implementation phase. The FDIC recently approved rules that establish clear standards for permitted payment stablecoin issuers (PPSIs). For your business, this means greater security: regulated issuers must now follow strict capital and risk management requirements tailored to their size. These rules also mandate that issuers generally redeem stablecoins within two business days, providing the predictable liquidity needed for enterprise treasury management.

Is the Hong Kong Stablecoin Ordinance fully operational for my Asian suppliers?

Yes. The regime came into full effect on August 1, 2025. It requires all fiat-referenced stablecoin issuers in Hong Kong to be licensed by the Hong Kong Monetary Authority (HKMA). This provides a regulated “green zone” for your payments to suppliers in the region. If you are paying vendors in Southeast Asia or Hong Kong, using HKMA-licensed stablecoins ensures you are transacting through entities that meet high standards for reserve management and anti-money laundering (AML) controls.

What are the specific IRS reporting requirements for stablecoins in 2026?

The IRS continues to treat stablecoins as property, not cash. This means every disposal—whether you are paying a vendor, converting to fiat, or swapping tokens—is a taxable event. Key updates for 2026 include:

- Form 1099-DA: Digital asset brokers now issue this form to report gross proceeds from your transactions.

- Wallet-by-Wallet Accounting: You must now track the cost basis for assets based on the specific wallet or account where they are stored, rather than using a universal pool across all your holdings.

- Fair Market Value: Your Salesforce records should automatically capture the USD value at the exact moment of receipt to establish an accurate cost basis for future reporting.

Does Stripe handle the blockchain technicalities for me?

Stripe now offers highly integrated stablecoin payout and settlement options that bridge the gap between fiat and blockchain. Their infrastructure allows you to initiate a payout in fiat, which is then converted to USDC and sent on-chain to your recipient’s wallet. This settles in minutes rather than days. Because Stripe manages the liquidity and network fees, your finance team doesn’t have to manage private keys or interact directly with decentralized exchanges, keeping your operational workflow within familiar dashboards.

Which networks and assets are dominating the market right now?

The stablecoin market cap reached a record of over 283 billion dollars by late 2025, with Tether (USDT) and USD Coin (USDC) remaining the primary leaders. While Ethereum carries a significant portion of the value, networks like Tron and various Layer 2 solutions have become the preferred choice for high-volume payments due to their lower transaction costs. When setting up your Salesforce payment flows, supporting these major assets ensures maximum compatibility with your global partners.

Final Thoughts

Stablecoins aren’t some distant blockchain fantasy anymore. In 2025, the market hit 300 billion dollars, and in 2024, transaction volume exceeded 27 trillion dollars. Real companies move real money through these networks today, and the trend accelerates as payment processors, banks, and fintech platforms invest in infrastructure. Fiat stablecoins in Salesforce integrate directly into your existing workflows through native solutions that require no custom code or blockchain engineers.

Implementation starts small and scales fast. You pick one use case-accepting payments from an international customer, paying a trusted vendor, or tracking a client’s crypto holdings-then validate the workflow before expanding. Your ERP already understands payments, reconciliation, and compliance, so stablecoins simply add a faster, cheaper rail that plugs into infrastructure you’ve already built. Success looks different for every organization, but the pattern holds: you reduce payment friction, improve working capital through faster settlement, cut correspondent banking fees, and gain operational transparency that traditional rails cannot match.

If you’re ready to explore how fiat stablecoins work with Salesforce for your organization, connect with Web3 Enabler to discuss your specific use case. We specialize in connecting blockchain technology with your existing corporate infrastructure through Salesforce Native solutions available on the AppExchange. Our tools are built for business operations, not crypto speculation.