Cross-border payments remain broken. Businesses lose millions annually to hidden fees, slow settlement times, and opaque processes that belong in the past century.

Cross-border payments remain broken. Businesses lose millions annually to hidden fees, slow settlement times, and opaque processes that belong in the past century.

We at Web3 Enabler have watched companies struggle with outdated banking rails while modern alternatives sit unused. This guide shows you what’s changed, why it matters, and how to move forward.

Why Traditional Cross-Border Payments Cost So Much

The Wire Transfer Fee Trap

Banks charge up to $40–$50 per international wire transfer, then add a currency conversion markup of 3–5% on top of the mid-market rate. A company sending $100,000 monthly loses an extra $3,000–$5,000 to that hidden markup alone. Intermediary banks along the SWIFT chain deduct their own fees, so the recipient receives less than you sent. A real payment might arrive $500–$2,000 short due to multiple intermediaries taking cuts.

These aren’t rare edge cases. They happen on nearly every cross-border wire because the SWIFT network connects over 11,000 financial institutions, and each one extracts fees. Traditional banking rails force you to accept whatever rate your bank offers and whatever fees they charge. You have no visibility into what happens between your bank and the destination, so you cannot optimize or challenge the deductions.

Settlement Speed Kills Cash Flow

SWIFT transfers commonly take 1–3 business days, sometimes longer depending on the destination country, compliance checks, and time zones. A payment that lands on Friday won’t clear until Tuesday. That five-day lag forces companies to hold cash reserves they’d rather deploy elsewhere. ABA wires offer same-day settlement within the US, but they cost more and don’t solve the international problem. ACH transfers are cheaper but take 1–3 business days and don’t work across borders.

Real-time or near-real-time tracking is missing from traditional systems, leaving finance teams to manually reconcile transactions and wonder whether a payment arrived or got stuck in compliance review. The uncertainty compounds the cost of waiting.

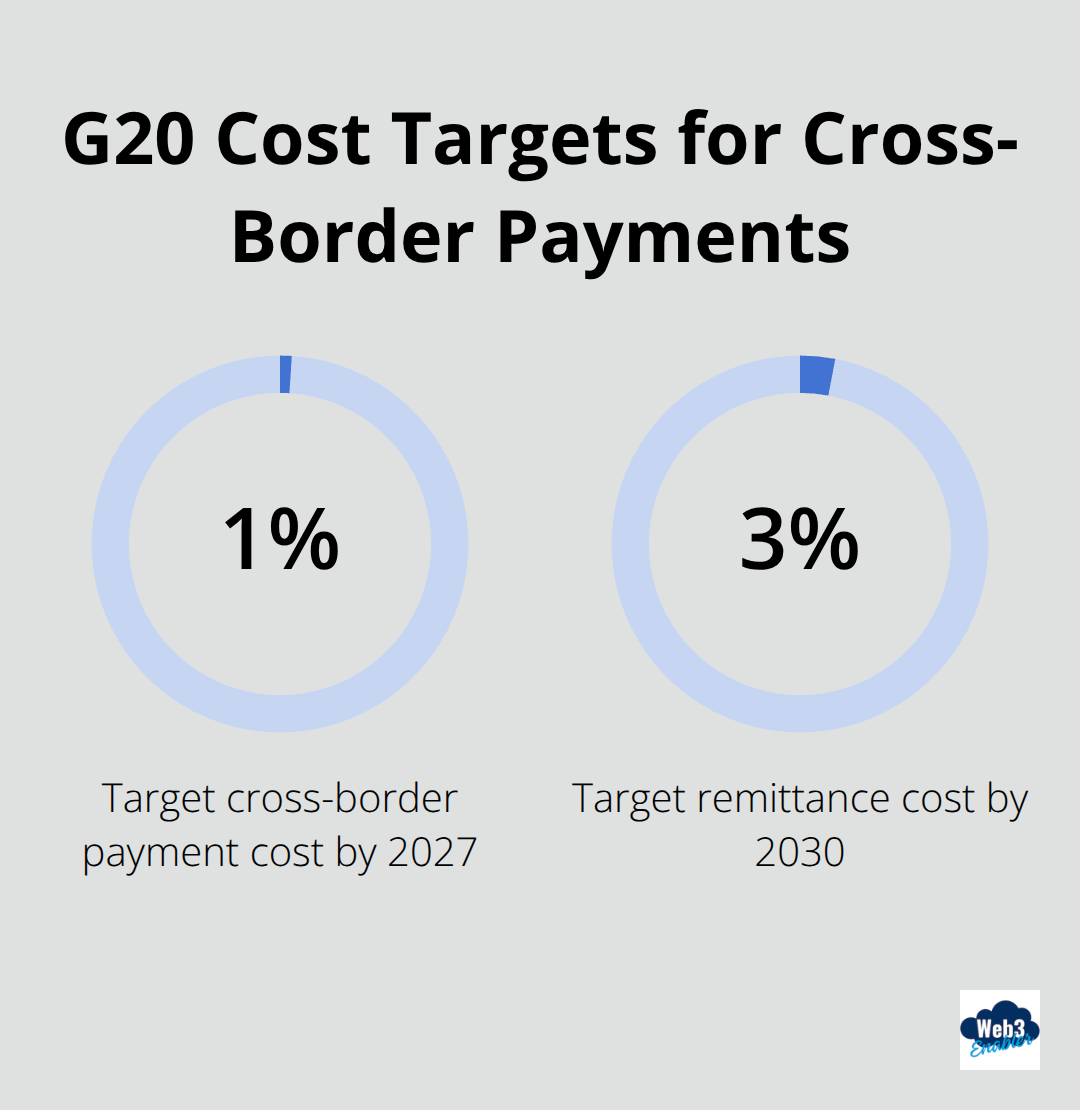

The Gap Between Goals and Reality

The G20 targets aim to cut cross-border payment costs to 1% by 2027 and remittance costs to 3% by 2030, yet current costs still exceed these goals by multiples. That gap exists because the traditional banking infrastructure wasn’t built for speed, transparency, or efficiency. It was built for control and intermediary revenue.

Modern alternatives now exist that address each of these pain points. The next section shows what has changed and why forward-thinking companies are moving away from SWIFT.

What Makes Modern Payment Rails Actually Work

Stablecoins and Blockchain Settlement Transform Speed and Cost

Stablecoins and blockchain settlement have moved from experimental to operational. Platforms like Slash support global transfers in 180+ countries and 135+ currencies, with native support for stablecoins USDC and USDT across 8 blockchains. On-ramp and off-ramp between fiat and crypto typically costs less than 1%, often making crypto transfers cheaper than traditional FX. Settlement happens in seconds to minutes on the blockchain. This isn’t theoretical-it’s how forward-thinking companies reduce cross-border costs from $40–$50 per wire plus 3–5% FX markup down to under 1% total. A $100,000 payment that costs $4,000–$5,000 via SWIFT costs under $1,000 via stablecoin rails.

Digital Platforms Offer a Middle Ground

Wise has shifted toward faster alternatives through partnerships with Morgan Stanley and Standard Chartered, enabling transfers in 1–2 business days instead of 3–5, with mid-market rates and no hidden markups. Real-time payment systems are expanding globally, with many territories implementing instant payment rails that eliminate the multi-day settlement lag entirely. The global B2B cross-border payments market reached $31.6 trillion in 2024 according to FXC Intelligence and is projected to grow to $50 trillion by 2032, driven largely by adoption of faster, cheaper rails. Companies still using SWIFT for routine payments essentially pay a tax on inefficiency.

Matching Payment Methods to Your Actual Needs

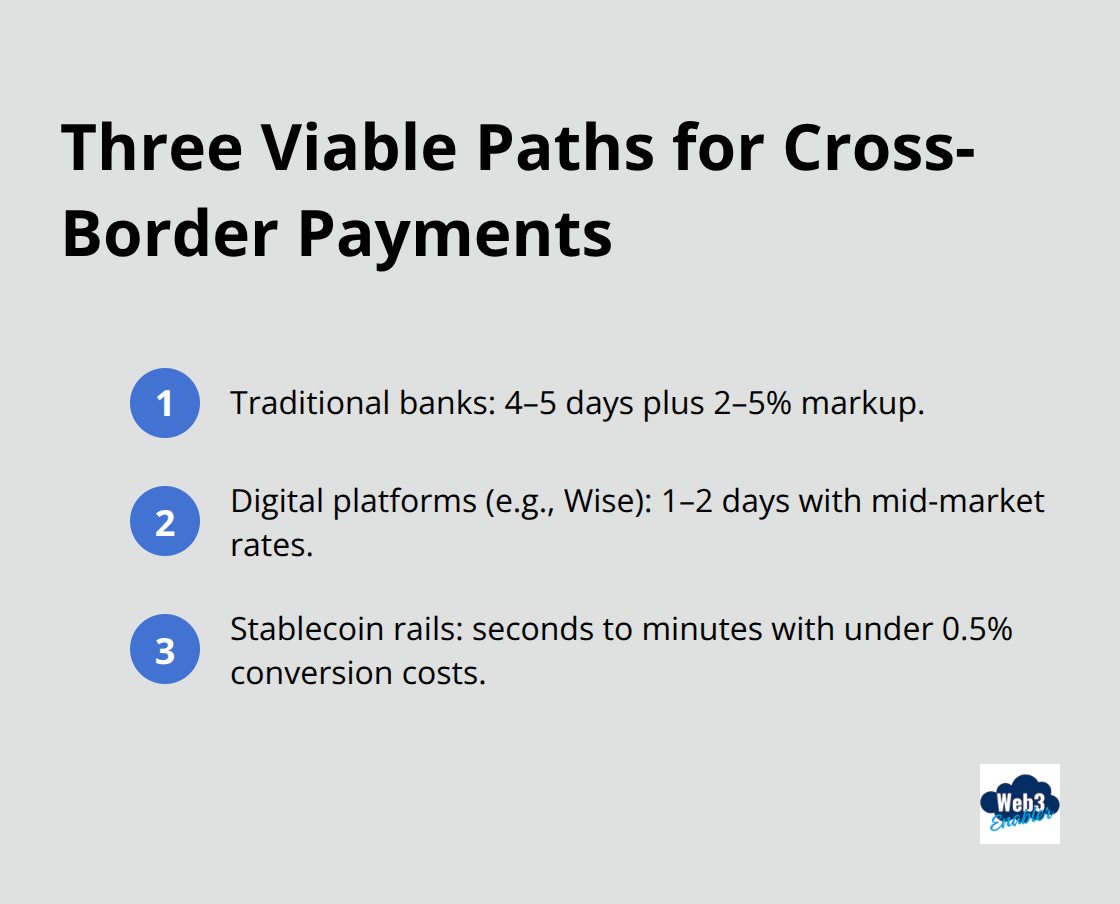

The practical choice comes down to what you pay and how fast you need it. For US domestic payments, ACH works when you have time and ABA wires work when you don’t, but neither solves international transfers. For cross-border, you now have three viable paths: use traditional banks and accept 4–5 days plus 2–5% markup, use digital platforms like Wise for 1–2 days with transparent mid-market rates, or use stablecoin rails for seconds to minutes with under 0.5% conversion costs.

Each path fits different situations-large payments to established vendors might justify a wire, recurring payments to multiple countries favor stablecoins, and everything in between fits the digital platform middle ground. The key is matching the payment method to your actual need rather than defaulting to whatever your bank suggests.

Integration and Scale Matter for Implementation

Integration matters too. Modern solutions need to connect with your existing accounting software, payment approvals, and reconciliation workflows. Solutions that plug into QuickBooks, Xero, Sage, or NetSuite save hours of manual work and eliminate reconciliation errors. Batch payment features matter for scale-if you pay 50+ vendors monthly, mass payment capabilities reduce administrative burden and cost per transaction significantly. The right platform handles these connections seamlessly, turning cross-border payments from a finance headache into a routine operation. Once you’ve selected the right rails and integrated them into your workflow, the next step is understanding how to implement these solutions without disrupting your existing operations or creating compliance risks.

Making Cross-Border Payments Work in Your Business

Connect Your Payment Rails to Existing Systems

Integration determines whether your payment strategy succeeds or fails. You can select the perfect payment rail, but if it doesn’t connect to QuickBooks, Xero, Sage, or NetSuite, your finance team spends hours reconciling transactions manually. Start by auditing your current accounting software and payment approval workflow. If your platform lacks built-in support for your chosen provider, APIs often fill the gap-verify this before committing. Test your integration in a staging environment with a small vendor payment first, not with your largest supplier. This approach prevents costly mistakes when you scale.

Automate Batch Payments to Save Time and Money

Batch payment capabilities matter more than most realize. If you pay 50 or more vendors monthly, mass payment features reduce administrative time by 70% or more compared to processing individual transactions. Real-time analytics dashboards help you track where money goes and how long settlement takes, giving you the visibility that traditional SWIFT transfers never provided. Automation also reduces the number of unique transactions you process, which lowers compliance friction and cost per payment.

Run Compliance Checks Without Causing Delays

Compliance and cost monitoring must happen simultaneously, not sequentially. AML and KYC checks should run automatically in the background rather than causing transaction holds that delay payments by days. Modern providers handle these checks without manual intervention, but older banking partners often don’t. Automate recurring payments to regular vendors-this reduces both cost and compliance friction because you process fewer unique transactions. The result is faster settlement and lower total cost per transaction.

Set Benchmarks and Monitor Performance

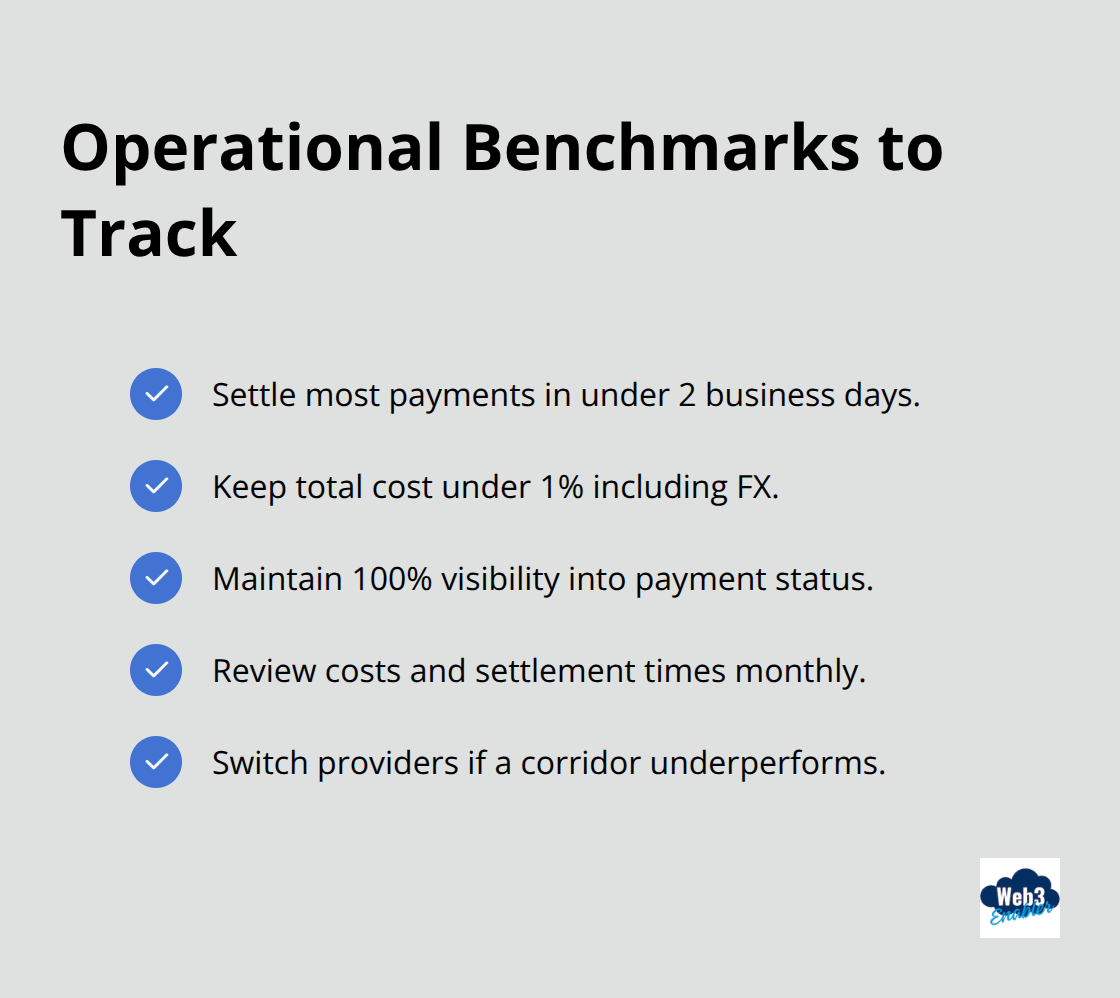

Try for settlement under 2 business days for most payments, under 1% total cost including FX conversion, and 100% visibility into where your money sits at any moment. According to FXC Intelligence, the global B2B cross-border payments market reached $31.6 trillion in 2024, and companies moving to faster rails report 15–20% improvements in cash flow within the first quarter.

Schedule monthly reviews of your transaction costs and settlement times against your benchmarks. If a corridor consistently costs more than expected or settles slower than promised, switch providers rather than accepting underperformance.

Treat Cross-Border Payments as a Strategic Cost Center

Companies that treat cross-border payments as a strategic cost center, not just a banking necessity, typically reduce annual cross-border expenses by 25–40% within 18 months. This shift requires discipline-you must measure performance, challenge underperformance, and continuously optimize your provider mix. The effort pays off through lower costs, faster cash flow, and reduced administrative burden across your finance team.

Final Thoughts

Modern cross-border payments deliver three concrete advantages over traditional banking rails: they cost less (typically under 1% total versus 4–5% through SWIFT), they settle faster (often in hours or 1–2 business days instead of 3–5), and they provide real-time visibility into where your money sits. Start by identifying your highest-cost payment corridors and test a modern solution on one corridor with a vendor you trust. Measure the cost, settlement time, and integration effort, then expand to other corridors if the results beat your current method.

Most companies moving to modern rails report 15–20% improvements in cash flow within the first quarter because faster settlement, lower fees, and reduced administrative time compound across dozens of vendors and multiple countries. Look for transparent pricing, broad currency coverage, reliable settlement speed, and seamless integration with your accounting software when selecting a provider. The companies winning in 2025 aren’t waiting for banks to modernize-they’re moving now.

We at Web3 Enabler specialize in connecting blockchain technology with your existing corporate systems to enable faster, more secure cross-border payments while maintaining full compliance and visibility. Our Salesforce Native solutions help businesses send global payments within their current setup without disruption. Explore how modern cross-border payment rails can transform your payment operations.